The COP29 summit in Baku highlighted significant gaps between climate ambitions and real-world outcomes, focusing on the New Collective Quantified Goal (NCQG) for climate finance. Despite raising the annual climate finance target to $300 billion, the amount falls far short of the $3 trillion needed annually for a global low-carbon transition. The summit's outcomes were criticized for insufficient transparency, inefficiencies in fund deployment, and disproportionate influence from 1,770 fossil fuel lobbyists overshadowing climate-vulnerable nations. Key challenges include bureaucratic delays, opaque financial tracking, and inadequate representation of underprivileged nations in negotiations. Critics emphasized the need for stringent conflict-of-interest policies to curb fossil fuel lobbying, alongside transparent Key Performance Indicators (KPIs) to ensure accountability in climate finance. While the NCQG presents an opportunity to mobilize global partnerships and private investment, its success hinges on equitable representation, robust monitoring, and effective disbursement. Without these, COP risks failing to meet its mission of achieving meaningful climate action.

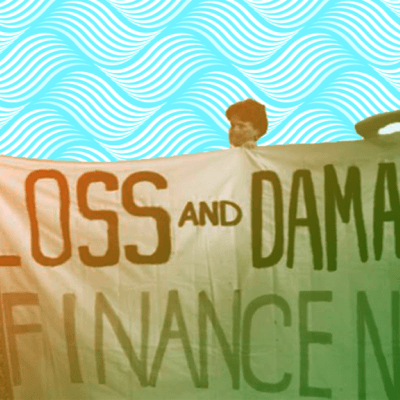

The Loss and Damage Fund, crucial for aiding vulnerable nations, will continue to struggle with implementation and funding. More closely integrating renewable energy will be key for climate adaptation.

Sub-Saharan Africa's access to flawed yet vital global carbon markets is challenging; initiatives like the Africa Carbon Market aim to refine these markets and spur economic growth. Integrating renewable energy into the evolving Loss and Damage Fund is key for effective climate adaptation in 2024.

In 2024, the demand for green minerals is reshaping global power, highlighting the need for a new Bretton Woods system to ensure sustainable, equitable growth and manage geopolitical and environmental challenges.

Today, French President Emmanuel Macron will host a Summit for a new global financing pact in Paris. Over 100 heads of state, policymakers, and international organizations will convene to discuss financing solutions to respond to global crises, including climate change, development, and biodiversity loss.

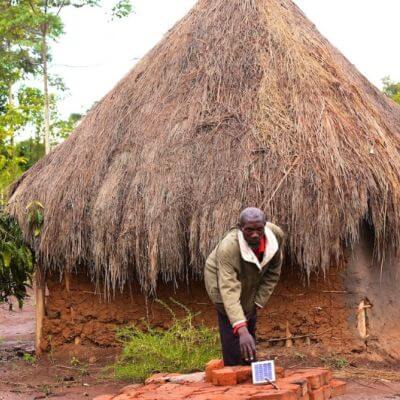

Platform for Energy Access Knowledge

Platform for Energy Access Knowledge Explore the best energy access idata and thinking with PEAK, our powerful interactive information exchange platform.