January’s arrival started the countdown on the last decade to achieve the UN Sustainable Development Goals (SDGs), which also means that it is once again time for the annual Power for All list of the top trends we expect to see in the coming year. You might also get a kick out of seeing how we did in our predictions for 2019 (by our count, we got 8 of 10 right, missing the mark on blockchain and small-scale wind).

One megatrend continues to be that our sector -- the decentralized renewable energy sector in emerging markets -- is scaling. While this is not “news”, it’s worth remembering. The markers of sector maturity are there (companies failing, increased merger & acquisition activity, etc), and this should be welcomed, not feared.

So, in no particular order, here’s what to look out for in 2020.

-

Country, my country: Real change occurs at the national and sub-national levels. The massive $350 million World Bank loan to Nigeria last year was the start of a trend that will see much greater momentum in 2020: well-funded, country-level programs. Togo, Ethiopia, Uganda, Madagascar, Mozambique, and many other countries will see more dedicated interventions. Nigeria’s success or failure is still to be determined and will continue to be highly scrutinized. Ethiopia will be a close second, given its size and potential impact. But we must not forget: more money and support at the country level assumes a country’s ability to absorb it, i.e. a viable market ecosystem. And that will be a major barrier. For more perspective, check out our 25x25 partnership.

-

New leadership, new direction: Most notably, the arrival of Damilola Ogunbiyi as the new CEO of SEforALL signals an injection of new energy and direction for the overall renewable energy movement, including access. A formidable fundraiser with an entrepreneurial, action-oriented DNA, we’ve had the pleasure of working closely with Ms. Ogunbiyi in Nigeria. It remains to be seen how that translates to the United Nations bureaucracy. Other leadership changes are happening too, at the world’s largest donor, the European Commission, which has a new head of energy, the dynamic Ditte Juul Jørgensen, and Stefano Signore, who took over on sustainable energy and climate change. We will also see new faces at Power Africa and REEEP.

-

Long live co-benefits: Nexus, co-benefits, dividends, productive use… whatever you call them, lip service about focusing on the outcomes of distributed renewables is finally turning into action. Instead of talking about energy to the energy sector, we’re finally starting to talk to the beneficiaries about the impact of distributed renewables on healthcare, agri-food, employment, education, connectivity, cooking, etc. It’s marketing 101: tell your customer how you can serve them better. We just worked with IRENA & ILO to launch the Sustainable Energy Jobs Platform, the World Health Organization (WHO) and others launched the Health & Energy Platform of Action (HEPA). More is needed and more is coming.

-

More sophisticated money: The sector’s growing maturity, and its more segmented and advanced supply chain mean that more targeted financial tools are needed to meet the next phase of growth. Mechanisms for de-risking and securitizing bundled portfolios will be key to leveraging larger pools of commercial and local capital. Based on initial work by the International Solar Alliance, the World Bank recently launched the Solar Risk Mitigation Initiative (SRMI) to mobilize $500 million in emerging economies. The African Development Bank meanwhile reformed its Sustainable Energy Fund for Africa (SEFA) with a greater focus on Results-Based Finance (RBF), which commercial investors are strongly demanding. Because of the smaller ticket size of our sector, more focus is also being placed on portfolio aggregation and securitization. Unlocking local currency will also progress.

-

Integrated electrification: Don’t forget policy and regulation. With more countries embracing mini-grids and home solar, government demand is growing for support on how to plan for the energy infrastructure of the future. This has spawned a growing community of practice working to help, including a huge army of consultants. Integrated electrification is a focus area of the new Global Commission to End Energy Poverty, and many others such as IRENA, the World Bank, WRI and SEforALL. Notably, DFID is finalizing a set of key principles for ensuring donor alignment vis-a-vis strategic energy planning. Additional focus is also emerging on the implementation gap that exists in putting plans into practice. Keep an eye out for emerging public-private partnership to bridge this gap, such as our Utilities 2.0 work in Uganda with Umeme, Konexa in Nigeria, and Tata Power in India.

-

e-Mobility: We’ve been talking about this for a while, but is 2020 the year? With battery costs continuing to fall, and so much action on efficient electrical appliances happening around energy access, it’s not a stretch to say that electric two-wheelers and three-wheelers are just bigger consumer appliances that also stand to gain from the ruthless quest for innovation. Cool start-ups are looking into this area, and foundations and donors are taking a closer look as well, including how EVs can take advantage of mini-grids (and vice versa), and the role of transportation in agriculture.

-

Going geospatial & digital: As discussed in a recent report, there is still enormous potential for digital technologies in emerging markets -- big data and AI, smart meters, IoT, geospatial sensing and remote management. This is a critical element in continued reductions in operating expense of sector companies, and an area where decentralized private sector companies will push bigger utilities into the future. Geospatial tools are also becoming a serious input into planning.

-

e-Cooking: This makes the list for the second year in a row. The arrival of the Modern Energy Cooking Services (MECS) program and a new $500 million clean cooking fund from the World Bank could be game changers, and work by Efficiency for Access, CLASP, the Clean Cooking Alliance and others will continue to push a new generation of products and business models.

-

Adaptation and resilience: What is going to be the most resilient energy infrastructure of the future as natural disasters (floods, fires, drought, storms) and climate change amplify? We found out in late 2019 that distributed renewables don’t have the strongest emissions reduction story (according to GIZ and RLI its just 870 million tonnes of CO2e by 2030). But, their new study also concluded that distributed renewables not only make communities more resilient both socially and economically, but also are more resilient compared to grid infrastructure. Governments and utilities around the world are waking up to this, in Puerto Rico, in California, in Australia. Our sector’s contribution to adaptation needs to be moved to the front of the climate discussion, as it becomes more apparent that we will miss the Paris agreement goals.

-

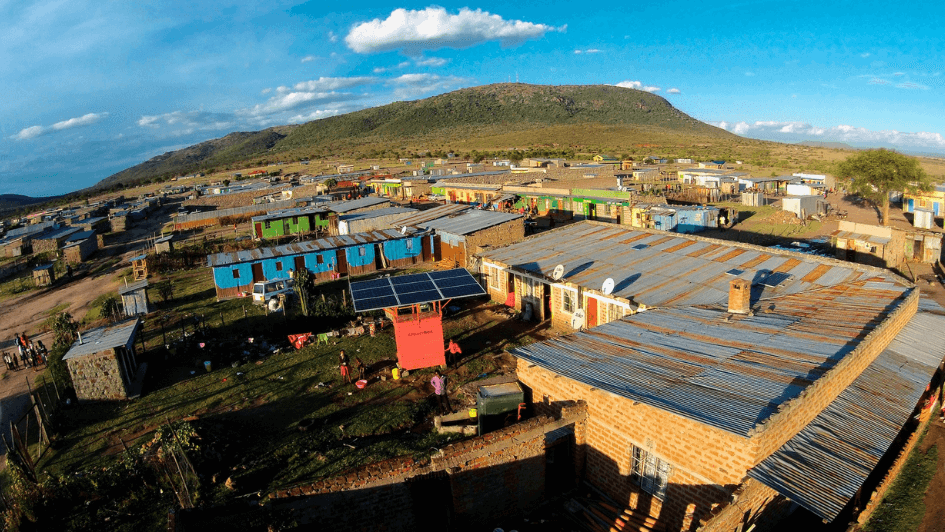

MPs getting renewable: Long under-utilized in the energy transition, parliamentarians are now emerging as another potential lever for accelerating access, thanks to the Global Renewables Congress, Climate Parliament and others, as well as the devolution of more energy planning to local governments. In Kenya, for example, counties have been given much more authority, leading to innovation in districts where local government is strong and progressive. This bottom-up dynamic could bode well for faster access gains if properly leveraged.

Did we miss something? Share your thoughts with us on Twitter @Power4All2025