India grabbed headlines in April 2015 when the Modi government pledged to achieve universal energy access, aka Sustainable Development Goal 7 (SDG7), in four years. It was and remains a world-leading commitment, and coupled with a 175 GW target for new clean power generation by 2022 (including 40 GW of grid-tied rooftop solar), it triggered a wave of new investment and market growth.

Yet it was primarily a vision of access from grid extension, and a closer look at progress to date reveals that more than just a national goal will be required to successfully achieve SDG7. India’s energy ministry has said that all villages will be electrified by the end of this year, and all homes in those villages by 2019. But the government definition of “electrified” is a controversial one — only 10 percent of homes must receive electricity for a village to count as electrified.

Questions have already emerged publicly over whether India will meet the 175 GW goal. And doubts persist about India’s ability to truly meet 100 percent, reliable energy access by 2019.

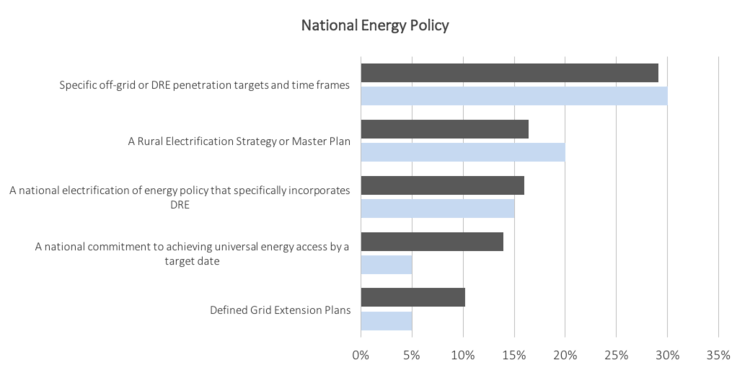

The issue, according to a recent Power for All survey of companies, is that a national target is not enough. While seen as a factor in the growth of decentralized renewable energy (DRE) solutions and achieving access, the survey showed that the number one national policy priority identified by DRE practitioners—by a significant margin—was setting a specific off-grid or decentralized renewable energy penetration target (and timeline); second was a rural electrification strategy; and third a national electrification policy that incorporates DRE.

One survey respondent explained that DRE penetration targets “communicate a clear action and commitment from the government and allow for relatively accurate forecasting of future growth potential.”

A recent example is that of Rwanda. In 2013 the country had only a few off-grid solar companies operating in it, with few households or businesses benefiting from distributed solutions. It was not until the government announced a specific DRE target of reaching 22 percent of the population with off-grid solutions by 2018, and adopted supportive policy measures, that DRE companies including Mobisol and BBOXX, as well as investors and the international community, stepped up their interest—and stepped into the country. The latest off-grid solar market sales report shows continuing upward growth in Rwanda’s distributed solar market, with a 53 percent increase in sales during the first half of 2016 alone.

Given that 250 million people in India lack energy access—making it the the world’s largest potential market for DRE—bolstering India’s high profile targets with specific targets for DRE penetration in rural markets would turbo-charge investment. Indeed, integrated planning that brings together grid and non-grid targets is key, particularly in the case of mini-grid developers.

As another survey respondent explained: “For mini-grids the key policy risk is grid integration. Hence a recognition that mini-grids are part of the national strategy rather than a bet against it is key.”

This is a critical point. India’s focus on a grid-dominated future has dampened investor interest in mini-grids. Why, investors ask, would I back a solution that will be obsolete once the grid arrives? Of course, this erroneous view makes the assumption—an assumption that is far from guaranteed with bankrupt utilities already struggling—that the grid will arrive and be reliable even if or when it does. Not to mention that decentralized solutions can be fed into a grid if the system is designed properly, as seen in more developed markets.

A target announced last year of 10,000 mini-grids in five years bodes well for India and is a commendable first step, as are state-level policies for mini-grids, but it’s still too early to know their impact. Moreover, while 40 GW has been carved out for rooftop solar, it is grid-tied only and mostly commercial and industrial rooftop in urban markets, while there has been no such carve out for distributed rooftop solar for rural India.

And this leads to the final observation: that “rural” is a broad term, and in places like India it has little meaning. India after all is a federalist system with 29 states that have considerable autonomy. Each of them has its own geography and resource profile, and each will need its own DRE policy. So while national access targets are good, and specific national DRE penetration targets are better, the best (and most important) target for DRE-led rural electrification—at least for some countries with federalist systems such as India and Nigeria—will need to come at the sub-national level.

"In India there is a tendency to fall into the trap of just liaising with the central government ministries when the real 'power' to act on power lies with the states," says Kartikeya Singh, deputy director US-India Policy Studies at Center for Strategic and International Studies.