Many hurdles remain, including low consumer awareness, lack of mobile money and a fragmented telecom industry, but Anna Wells, senior communications adviser at GOGLA, reports that momentum is growing heading into 2018

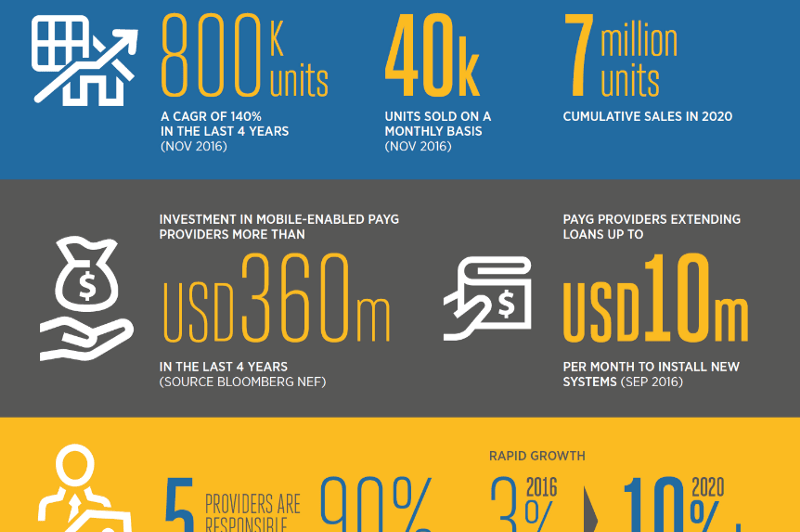

Pay-as-you-go (“PAYG” or “paygo”) is a way for energy consumers to purchase products or services in small increments. PAYG solar home solutions have exploded in rural Africa in recent years, with a diverse set of business models, including: rental, ‘lease-to-own’ (when customers pay small amounts until they own a system fully), upfront sales with financing partners and direct cash sales.

With 300 million people in India still without electricity, industry leaders met recently in Mumbai at an event co-organized by GOGLA, IFC Lighting Asia / India and GSMA, to explore opportunities. Participants included PAYG and distribution companies, mobile wallet companies, and digital finance solutions (or DFS) providers.

Current landscape for PAYG in India

India is a cash-based economy and, unlike the African market, mobile money is not yet widely used. There is huge potential for a PAYG market in India and this approach has several key benefits: it increases the affordability for the customer, it provides companies with a direct link to their customers, and allows up-selling and cross-selling of various products to the same customer to help them climb the energy staircase. PAYG also provides some degree of insurance to the customer against faulty products.

Despite the clear benefits, the PAYG market in India and across South and South-East Asia is in its infancy compared to other markets, and faces several challenges and risks. Key issues are that PAYG is 1. capital intensive, 2. subject to policy fluctuations and 3. complicated to operationalize on the ground.

The market is a complex one, and specifically the question around why there has been a slow uptake in PAYG solar in South and South-East Asia was discussed as a central topic among the companies. Kerosene subsidy programs have a major impact on the market, and efficient alternate channels were also cited as having some influence.

In addition, although mobile money is one of the key components to unlocking PAYG, the ecosystem of mobile money is very different in Asia than it is in East Africa. For example, M-Pesa is used widely across Kenya and Tanzania but is not yet used in any significant volume in India. Instead, a number of key mobile operators in India (Airtel, Idea, Vodafone and Jio) are starting to roll out payment banks. The environment is a different one in India too as not only is there low-level usage of mobile money, but there is also very little awareness of it.

Scaling up the PAYG market in India

According to executives at the meeting, keys to scaling PAYG in India include consumer level awareness; there needs to be a push to increase awareness of the services and of digital literacy. Also, from the service providers side improving last-mile distribution will be a key factor in scaling PAYG, and finding ways of collecting payment efficiently and effectively. From an infrastructure perspective, there is still poor network connectivity in rural areas for mobile phones.

While the challenges are great, the opportunities are vast — from joint opportunities for digital finance services and solar companies, to joint expansion programs to cover common geographies, leveraging bank business correspondent networks and distributor entrepreneur networks. There is also scope for marketing which is mutually supportive, for collaboration in increasing consumer education and improving customer services by players in the same space.

While the lack of mobile money in India has been a big challenge in adoption of PAYG, companies are nonetheless accelerating the growth of networks and cash-in cash-out points.

The payment landscape in India is changing very fast and therefore there needs to be continued work on awareness and communications around payment collection methods, as well as awareness of the customer of what options are available to him or her.